Library

Back to overview

Member documents

Trustee documents

Forms

Member updates

Jargon Buster

2026 Scheme Guide

2025 Actuarial report

Statement of Investment Principles 2025

Engagement Policy Implementation Statement 2025

TCFD Report 2025

2025 Report and Accounts

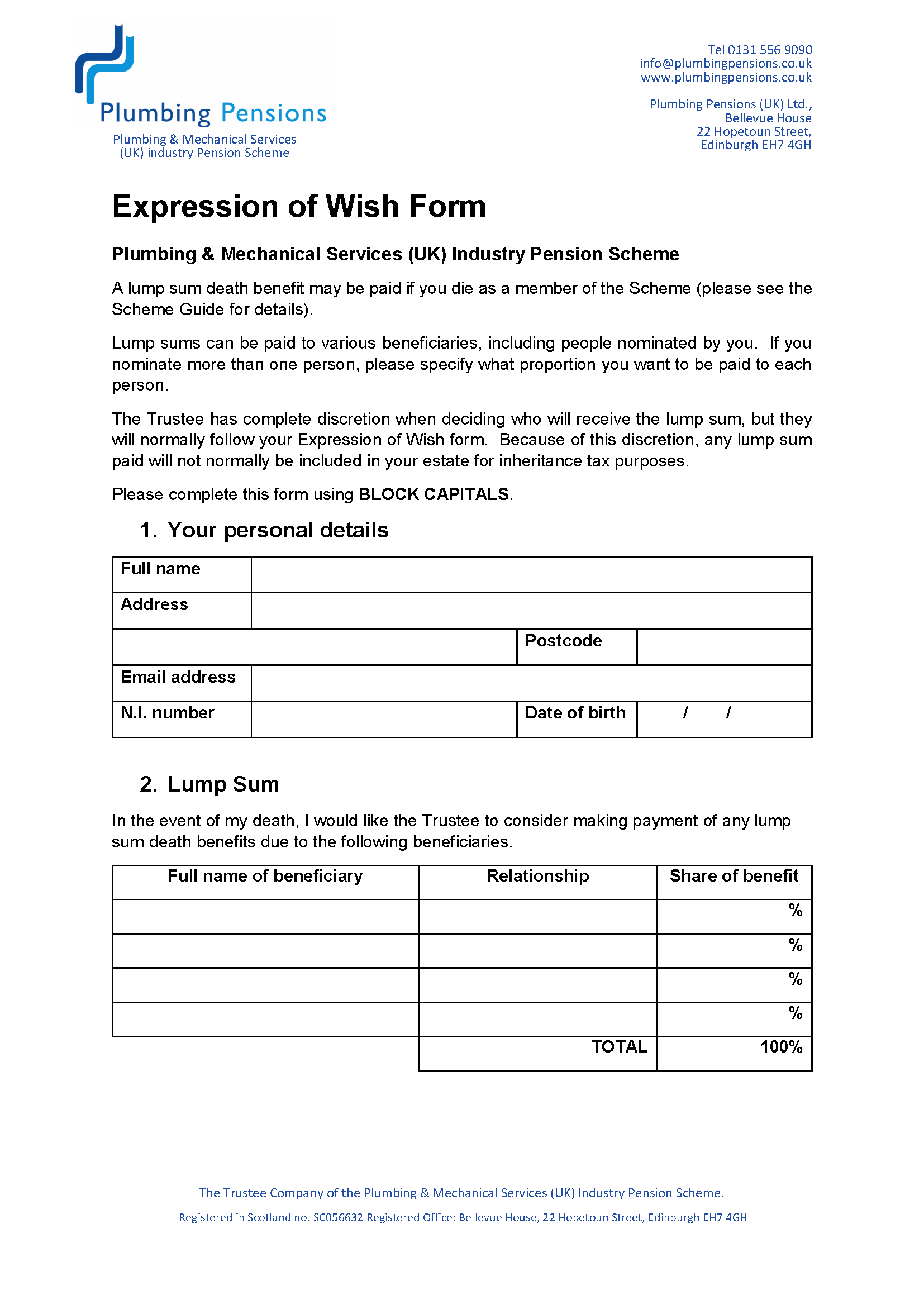

Expression of wish

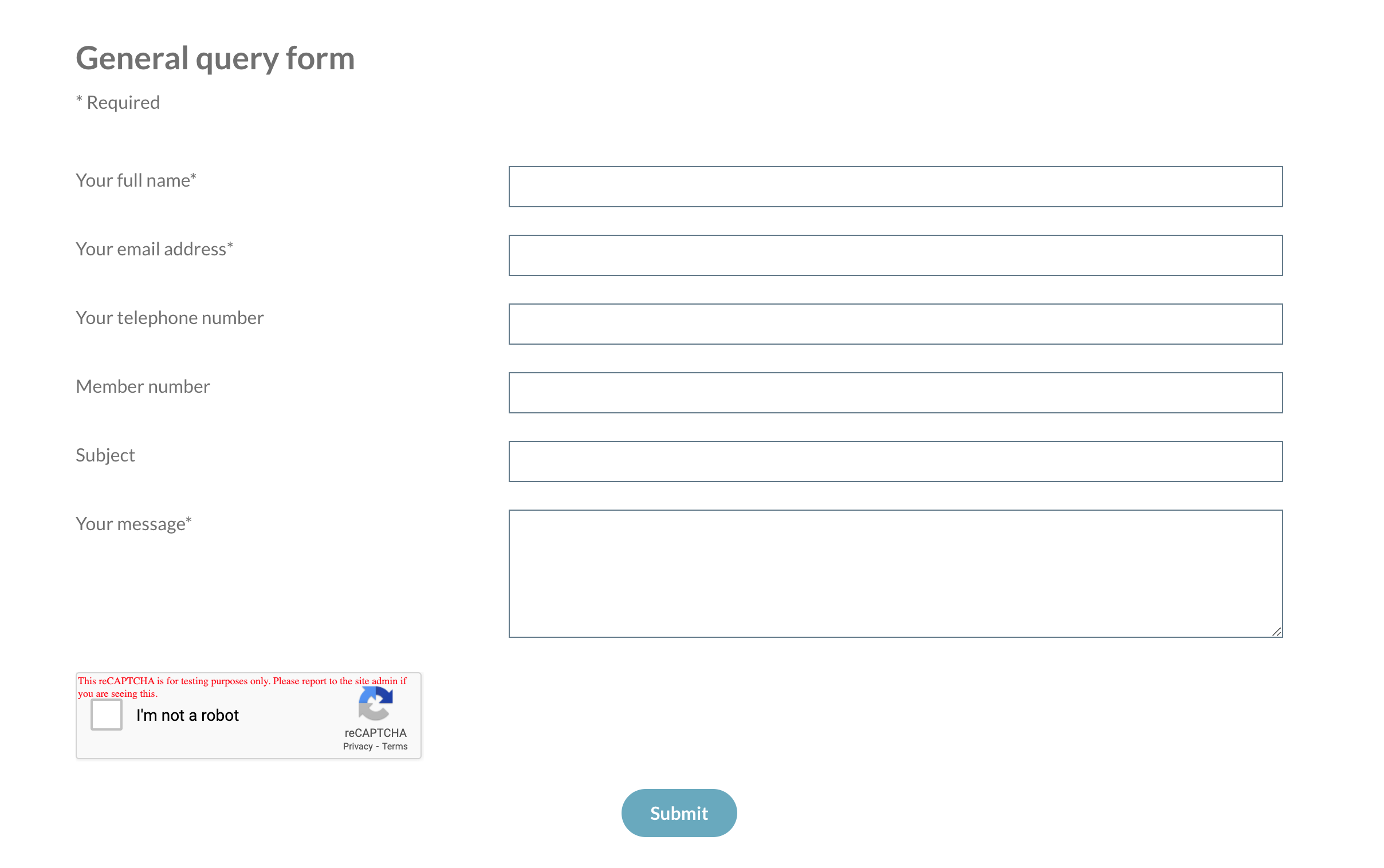

General query form

.png)

Member complaint form

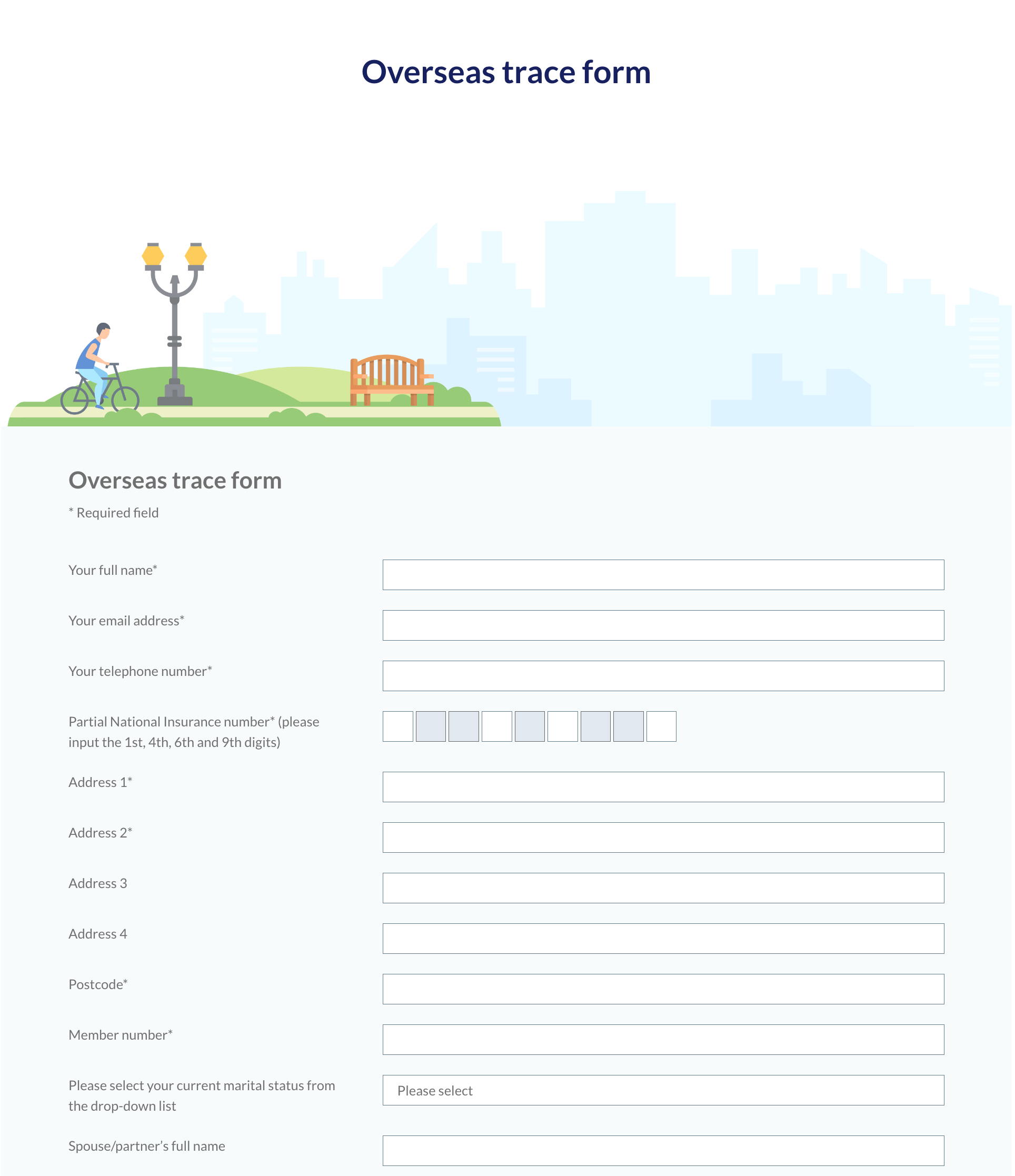

Overseas trace form

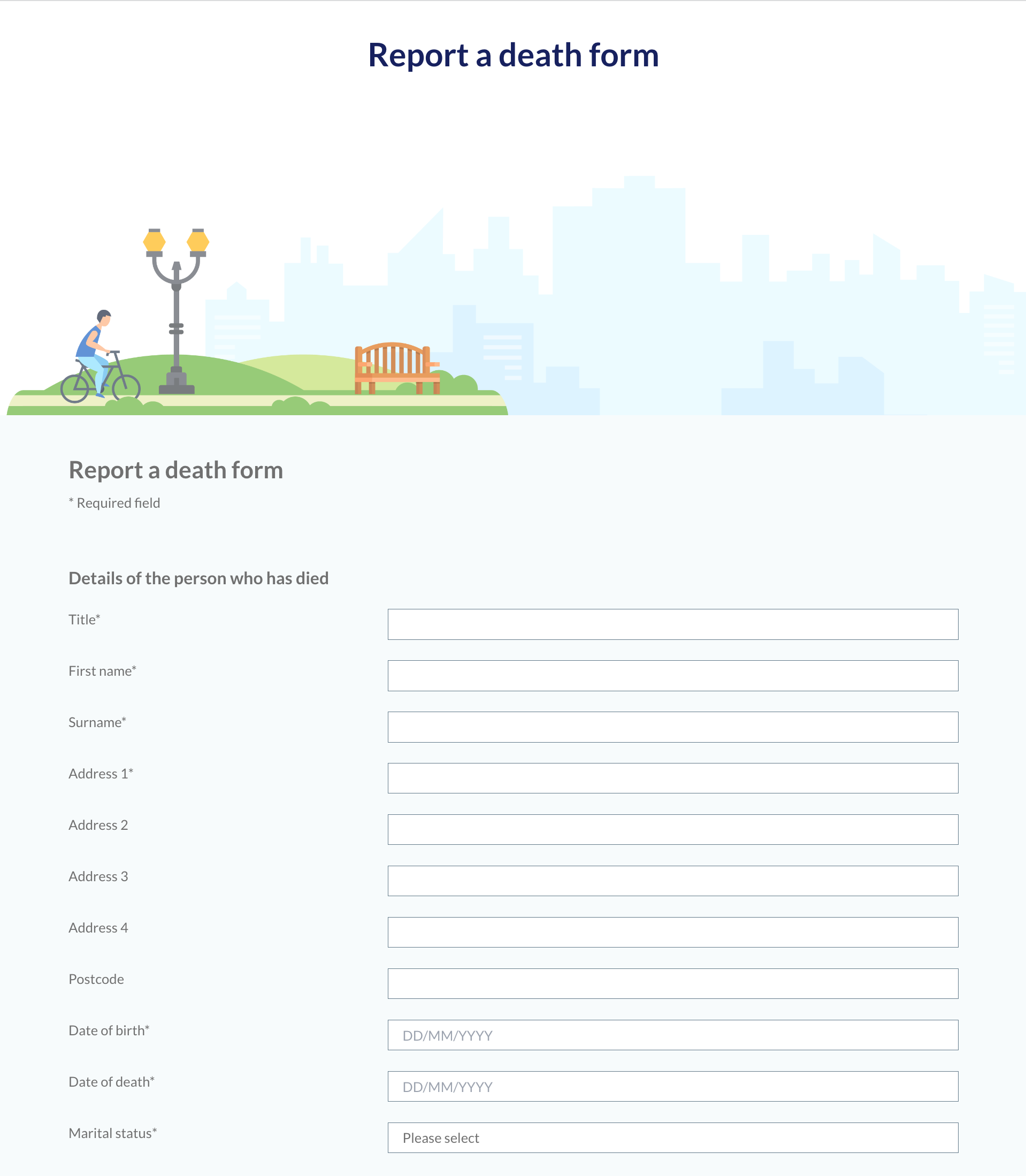

Report a death

Update details form

Member update 2025

Member Update 2024

Member Update 2023

Member Update 2022

Member Update 2021

Member Update 2020

Member Update 2019

Annual Allowance

The maximum amount you can save towards your retirement each year without incurring a tax charge. You can carry forward unused Annual Allowance from the previous three tax years.

Benefit scale

The basis on which you accrued benefits under the Scheme. There are five benefit scales: the 2017 scale, the Basic scale and three Higher Benefit scales.

Closure Date

The Scheme closed to future accrual from 30 June 2019. Contributing members stopped paying contributions or accruing benefits after this date.

Deferred member

A member who left pensionable service on the Closure Date or earlier, but has yet to claim their pension.

Dependant

Anyone who is financially dependent on you or was so dependent at the time of your death. The decision of the Trustee as to whether a person is your dependant is final.

Guaranteed Minimum Pension (GMP)

This is approximately the pension you would have earned under what was formerly known as the State Earnings Related Pension Scheme (SERPS) prior to 6 April 1997 if you had not been ‘contracted-out’ of it Unless stated otherwise, GMP is included in any pension figures given to you.

HMRC

HMRC means HM Revenue and Customs.

HMRC tax limits

If you think you might be affected by HMRC Tax Limits (the Annual Allowance and Lifetime Allowance) you should contact an independent financial adviser.

Incapacity

Physical or mental illness which stops you from continuing to work in any capacity or any trade for which you receive profit or pay. The Trustee’s decision as to whether you are suffering from incapacity is final.

Lifetime Allowance (LTA)

This is a limit on how much pension entitlement you can build up in your lifetime without incurring a tax charge on your retirement or death. It is measured against the value of your pension benefits from all your pension arrangements, not just the Scheme. The Government has removed the Lifetime Allowance tax charge with effect from April 2023 and the LTA was removed from April 2024.

Lump Sum Allowance (LSA)

This is a limit on how much lump sum you can take in your lifetime without incurring a tax charge on your retirement. It is measured against the value of all your Pension Commencement Lump Sums and tax-free elements of any Uncrystallised Funds Pension Lump Sums from all your pension arrangements, not just the scheme.

Lump Sum and Death Benefits Allowance (LSDBA)

This is a limit on how much lump sum and death benefits you can receive without incurring a tax charge. All authorised lump sums and authorised lump sum death benefits from all your pension arrangements, not just the scheme, count towards the LSDBA.

Normal Retirement Date

Your 65th birthday or any other date that the Association, the Federation and the Union agree is your Normal Retirement Date.

Pensionable service

Service while you were contributing to the Scheme.

Service

Service means employment with an employer participating in the Scheme. All contributing members were treated as having left service in the Scheme from the Closure Date.

Scheme year

A period of 12 months ending on 5 April.

State Basic Pension

If you reached State Pension Age before 6 April 2016 and you paid enough National Insurance contributions, you will receive the State Basic Pension from State Pension Age.

State Pension

If you reached State Pension Age on or after 6 April 2016, you will receive the flat rate State Pension, which replaced the State Basic Pension and the State Second Pension.

State Pension Age

This is the earliest age you can claim your State Pension. Your State Pension Age depends on when you were born. State Pension Age for men and women is currently age 66, but will gradually rise to age 67 from May 2026 for people born on or after April 1960. Under current legislation, State Pension Age will continue to rise further in the future. Irrespective of when you reach State Pension Age, your pension from the Scheme is payable from your Normal Retirement Date.

State Second Pension (S2P)

This was an additional amount of State pension based on a worker’s earnings. You will not have built up any rights to the State Second Pension while you contributed to the Scheme, because the Scheme was ‘contracted-out’ of the State Second Pension.

Uncrystallised Funds Pensions Lump Sum (UFPLS)

An uncrystallised funds pension lump sum is an authorised lump sum payment to a member from uncrystallised funds held in a money purchase arrangement. 25% of the UFPLS is tax-free with the remaining 75% taxable as income.